| Label | Value |

|---|---|

| Topic | Micron Technology (NASDAQ: MU) stock volatility and sell-off events in 2026 |

| Key Figures | Q2 FY2026 EPS: $12.20 (beat est. $8.50); Revenue: $23.86B; Stock 52-week range: $90.93–$916.76 |

| Who It Affects | Retail and institutional investors, semiconductor sector participants, AI/data center stakeholders |

| Time Period | March – May 2026 (most recent price: ~$902 as of May 26, 2026) |

| font-weight:bold;”>Bottom Line | Despite periodic sell-offs, MU’s AI-driven fundamentals remain strong, with 30+ analysts maintaining a Buy rating and UBS raising its price target to $1,625. |

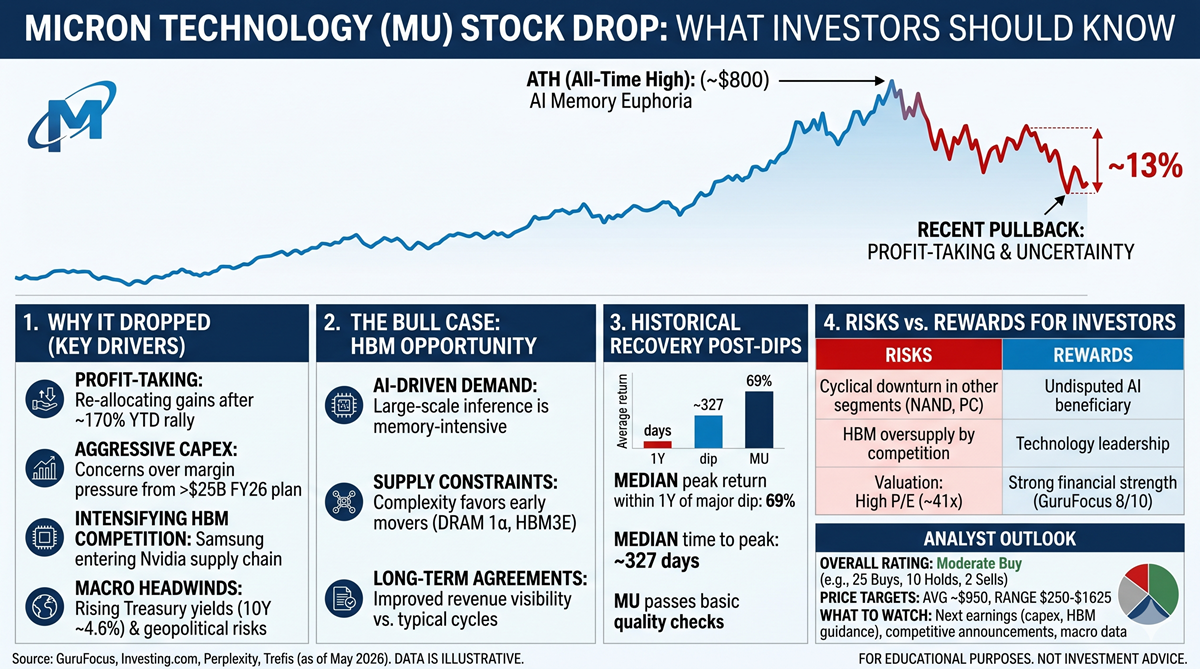

Why Did Micron Technology Stock Drop?

The Micron Technology stock drop has puzzled many investors who expected nothing but good news after the company posted one of the most impressive earnings beats in semiconductor history. Micron Technology (NASDAQ: MU) reported fiscal Q2 2026 earnings per share of $12.20 — shattering analyst estimates of $8.50 by more than 40% — and yet the stock still fell sharply in the days that followed. This apparent contradiction is at the heart of what investors need to understand right now. Whether you’re already holding MU shares, watching from the sidelines, or thinking about buying the dip, this article breaks down exactly what happened, why it happened, and what to realistically expect going forward.

Background: The Road to the Sell-Off

Micron’s story in recent years has been defined by a single mega-trend: the explosive demand for memory chips driven by artificial intelligence. Data centers powering large language models, cloud computing infrastructure, and AI accelerators have all required massive quantities of high-bandwidth memory (HBM) and advanced DRAM — products that Micron specializes in.

Leading into 2026, Micron’s stock had already surged more than 300% over the prior year, pushing valuations to levels that left little room for error. The stock’s 52-week low was $90.93, and by late May 2026 it had climbed past $900 per share. That extraordinary run created a double-edged situation: strong fundamentals, but equally strong expectations. Any hint of future uncertainty was always going to be magnified by such a stretched valuation, and that is exactly what triggered the periodic sell-offs that rattled investors during the first half of 2026.

What Actually Caused the Stock to Drop?

1. “Sell the News” Reaction After Record Earnings

Micron delivered spectacular Q2 FY2026 results: revenue of $23.86 billion against a consensus estimate of $18.90 billion, and EPS of $12.20 against an estimate of $8.50. By any objective measure, these were blockbuster numbers. Yet the stock fell in the days following the March 18, 2026 announcement. This counterintuitive reaction — often called a “sell the news” event — happens when so much good news is already priced into a stock that even outstanding results can’t push it higher. Investors who bought in anticipation of strong earnings simply took profits once the report was released.

2. Capital Expenditure Alarm Bells

A key driver of investor concern was Micron’s elevated capital spending outlook. The company raised its fiscal 2026 capital expenditure forecast to above $25 billion — roughly $5 billion higher than its previous guidance — citing aggressive expansion plans in Taiwan and accelerated construction at its Idaho and Virginia facilities. While this spending is necessary to meet surging AI memory demand, it signals heavier near-term costs and raised questions about free cash flow generation in the short run. For investors focused on near-term profitability, that was reason enough to reduce exposure.

3. Competition and Geopolitical Risk

Broader competitive pressures also weighed on sentiment. Samsung and SK Hynix are both investing heavily in high-bandwidth memory technology, raising the possibility that Micron’s current pricing power could erode as more supply enters the market. Additionally, geopolitical concerns — including discussions in South Korea about a potential windfall tax on AI companies — briefly rattled investors, who worried that similar policies could spread to other countries where Micron operates, including China. A broader semiconductor sector sell-off driven by valuation reassessments added further downward pressure, with trading volume during the steepest drop running approximately 33% above the three-month average.

📌 Key Points at a Glance

- Micron’s Q2 FY2026 earnings demolished estimates — $12.20 EPS vs. $8.50 expected, and $23.86B revenue vs. $18.90B expected — yet the stock still dropped post-earnings in a classic “sell the news” event.

- Elevated capex guidance of over $25 billion for FY2026 raised short-term profitability concerns among investors, even though the spending is designed to capitalize on long-term AI demand.

- Increasing competition from Samsung and SK Hynix in the high-bandwidth memory market, along with geopolitical risk, contributed to periodic sell-offs throughout early 2026.

- Despite the volatility, over 30 Wall Street analysts maintain a Buy or Strong Buy rating on MU, with UBS raising its price target to $1,625 on May 26, 2026.

- Analysts project a 611% increase in Micron’s earnings per share for the full fiscal year, underpinned by explosive DRAM pricing growth and surging AI server demand.

Impact and Analysis: What This Means for Investors

In the short term, investors should expect Micron’s stock to remain volatile. Memory stocks are inherently cyclical, and the speed of MU’s ascent means any stumble in demand data, supply news, or macro sentiment can produce outsized drops. The upcoming fiscal Q3 2026 earnings report — expected on June 24, 2026, with an EPS estimate of $19.11 — will be a critical test. If Micron can again beat expectations by a wide margin, it would validate the bull case. If guidance disappoints, another leg lower is possible.

Over the longer term, the fundamental picture looks compelling. Contract DRAM prices are projected to rise 58% to 63% in the current quarter, and full-year DRAM price growth of 125% has been forecast by research firm Gartner. Micron’s new 256GB DDR5 RDIMM product is specifically designed for AI servers, aligning the company directly with where data center investment is flowing. With the stock trading at what some analysts describe as a remarkably low forward multiple for its growth rate, institutional investors may view any significant dip as a buying opportunity rather than a warning sign.

People Are Also Asking

Conclusion: Volatility Doesn’t Change the Bigger Picture

The Micron Technology stock drop, viewed in isolation, looks alarming. But when placed in context — against record earnings, surging AI memory demand, aggressive capacity expansion, and overwhelmingly bullish analyst sentiment — it reads more like a natural pause in an extraordinary run than a fundamental breakdown. Micron is not a company in trouble; it is a company navigating the complex expectations that come with being one of the hottest stocks in the market.

For investors, the key takeaway is this: understand what you own, respect the volatility, and don’t let short-term price movements cloud your view of the long-term thesis. If you found this article helpful, consider sharing it with a fellow investor or leaving a comment with your thoughts on MU’s outlook for the rest of 2026.

Disclaimer: This article is for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any security. All data referenced was current as of May 27, 2026. Investors should conduct their own research and consult a qualified financial advisor before making investment decisions. Past performance is not indicative of future results.

Sources: Investing.com, 24/7 Wall St., Robinhood Markets, Public.com, Yahoo Finance, MarketBeat, Motley Fool, CNN Markets, Capital.com.

Related Internal Links

- Glucotil Reviews 2026 | Does It Really work? Find Now

- US Military Strikes on Iran: What Happens Next? (2026)

- AMD Stock Surges in 2026 — Should You Buy AMD Now?

- Lenovo Records Best Earnings as AI Revenue Nearly Doubles 2026