Introduction

If you’ve ever wondered whether it’s actually possible to save $1000 in 30 days, the short answer is yes — and it doesn’t require a six-figure salary to do it. This 30-day money saving challenge is designed to help everyday people find hidden savings in their current spending, make smarter financial decisions, and build real momentum toward bigger financial goals. Whether you need an emergency fund, want to wipe out a small debt, or simply want to prove to yourself that you can do it, this challenge gives you a clear, practical roadmap to follow. In a world where rising costs are squeezing household budgets from every direction, having a structured savings plan has never been more relevant.

Background & Context

Money-saving challenges have been popular in personal finance communities for over a decade, with formats ranging from the well-known 52-week savings challenge to no-spend months and the penny-a-day method. The concept of saving a specific dollar amount in a compressed time frame — like $1,000 in 30 days — gained renewed popularity as inflation rose sharply in recent years, pushing more households to look for ways to stretch their income further.

According to financial research, a large share of Americans cannot cover an unexpected $1,000 expense without borrowing money or going into debt. That single statistic has made the $1,000 savings milestone a culturally significant target — it’s roughly the amount needed to handle most common financial emergencies without resorting to credit cards or payday loans. The 30-day format works because it’s short enough to feel urgent and motivating, yet long enough to allow meaningful behavior changes to take effect. Social media communities around savings challenges have also helped keep participants accountable and engaged throughout the month.

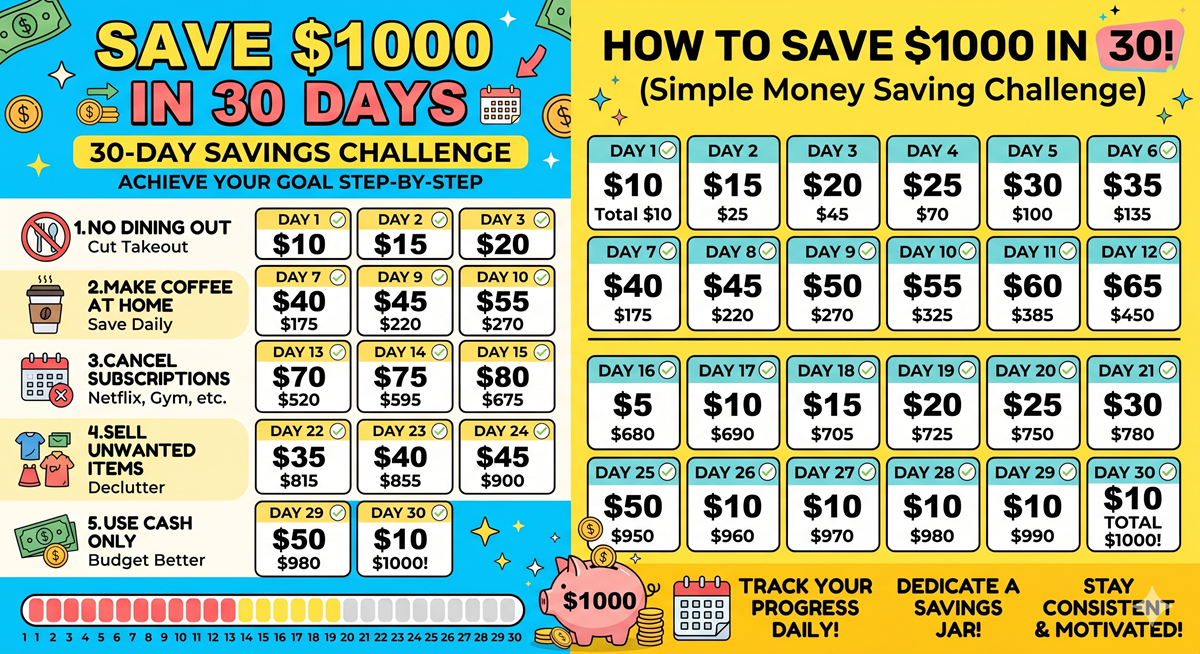

How to Save $1000 in 30 Days: The Full Breakdown

Step 1 — Set Up Your Savings System Before Day One

Before the challenge officially begins, the most important thing you can do is create a dedicated savings space. Open a separate savings account — ideally a high-yield savings account that earns interest — and label it your “30-Day Challenge Fund.” The psychological effect of keeping this money visually separated from your everyday spending account is enormous. It reduces the temptation to dip into the fund and gives you a clear, visible number to watch grow each day.

Next, calculate your daily savings target. To hit $1,000 in 30 days, you need to average roughly $33.33 per day. But this doesn’t mean you need to transfer exactly $33 every single day. Some days you’ll save more, and some days you’ll save less. What matters is that you hit the cumulative total by day 30. Write down your target, post it somewhere visible, and set weekly check-ins with yourself to track your progress.

Step 2 — Find the Money: Cut, Sell, and Earn

Most people are surprised by how much money is already flowing out of their accounts on autopilot. Start week one with a full audit of your last 30 days of bank and credit card statements. Look specifically for recurring subscriptions you’ve forgotten about, dining and takeout spending, impulse purchases, and any memberships you rarely use. Canceling just two or three unused subscriptions can free up $30–$60 per month instantly.

Selling unused items is one of the fastest ways to generate a lump sum early in the challenge. Go room by room through your home and identify clothes, electronics, furniture, books, sports equipment, or anything else gathering dust. Platforms like Facebook Marketplace, eBay, and local buy-sell apps make it easy to list items and get paid within days. Even a moderate cleanout can realistically generate $100–$300 toward your goal within the first week.

On the income side, consider small ways to boost your earnings during the 30-day period. Picking up a few extra hours at work, offering a skill-based service to neighbors (lawn care, pet sitting, tutoring, errands), or taking a short-term gig through delivery or task-based apps can add meaningful dollars to your challenge fund without requiring a long-term commitment.

Step 3 — Daily Habits That Add Up Fast

The day-to-day habits you practice during the challenge are what separate people who hit $1,000 from those who fall short. Cook meals at home instead of eating out — the average restaurant meal costs $13–$20 compared to roughly $4–$6 when cooked at home. Make coffee at home instead of buying it daily. Use grocery store loyalty programs, digital coupons, and store-brand products to reduce your weekly food bill by 15–25%.

Implement a “pause and wait” rule for any non-essential purchase over $20. Before buying, wait 24 hours. In most cases, the urge passes and the money stays in your account. Fill your calendar with free or low-cost activities during the month — parks, libraries, free local events, and time spent with friends at home rather than at restaurants or bars can replace spending with experiences that cost little to nothing.

⭐ Key Points

- Saving $1,000 in 30 days requires an average of just $33.33 per day — a realistic target for most working adults with a structured plan.

- Opening a separate, dedicated savings account is one of the most effective psychological tricks to stay on track and avoid spending the money.

- Auditing your subscriptions, dining habits, and impulse purchases in week one can reveal $100–$300 in savings you didn’t know you had.

- Selling unused household items on platforms like Facebook Marketplace or eBay can generate a fast lump sum early in the challenge.

- Daily cooking at home, skipping coffee shop visits, and applying a 24-hour pause rule before purchases are the habits that compound into big savings over 30 days.

Impact & Analysis

The immediate impact of completing this challenge is obvious — $1,000 in the bank. But the longer-term impact is arguably even more valuable. People who complete a 30-day savings challenge almost universally report that the experience changes how they see their own spending. They discover they had more financial flexibility than they realized, and they develop specific habits — cooking at home, auditing subscriptions, applying waiting periods before purchases — that continue generating savings long after the challenge ends.

In the short term, reaching $1,000 in savings creates a basic financial cushion that removes the anxiety of unexpected expenses. In the long term, people who use this challenge as a reset point often go on to build three-to-six-month emergency funds, pay off consumer debt faster, or redirect the habits learned here toward investing and wealth building. The 30-day structure is valuable not just as a one-time event, but as a repeatable model that can be applied every time a specific financial goal needs to be reached quickly.

People Are Also Asking

Conclusion

The 30-day $1,000 savings challenge works because it’s specific, time-bound, and built on habits that are entirely within your control. By auditing your spending, cutting what you don’t need, selling what you don’t use, and making small but consistent daily choices, you can reach a meaningful financial milestone in a single month. The process also rewires how you think about money — making you a more intentional spender long after the challenge is over.

If you’re ready to save $1000 in 30 days, start today: open a dedicated savings account, review last month’s bank statements, and commit to just day one. The rest will follow. If this guide helped you, share it with a friend who could use a financial reset — sometimes the best thing you can do for someone is show them that change is possible, one day at a time.

This article is for informational purposes only and does not constitute professional financial advice. Results will vary based on individual income, expenses, and financial circumstances. Always consult a qualified financial advisor before making significant changes to your financial plan.

Sources: General personal finance best practices, consumer spending research, and savings challenge methodology used by financial education communities.

Related Internal Links

- How to Lower Blood Pressure Naturally in 2026

- Best Ways to Make Money Online in 2026: Proven Methods

- How to Fix WiFi Not Working on Windows 11 (2026)

- US Gas Price Hits $4.56 — How to Save Money on Fuel in 2026