US Economy Update June 2026: Where Growth, Jobs, and Inflation Stand Right Now

| Label | Value |

|---|---|

| Topic | US Economic Performance and Outlook, Mid-2026 |

| Key Figures | GDP growth ~2.0–2.4% (2026 forecast); Unemployment ~4.5–4.8%; Inflation ~2.7% |

| Who It Affects | All American consumers, workers, businesses, and investors |

| Time Period | Q1–Q2 2026 data; Full-year 2026 projections |

| Bottom Line | The US economy is expanding at a steady but moderate pace, with resilient business investment offsetting lingering inflation pressures and global uncertainties. |

Introduction

The US economy update for June 2026 arrives at a pivotal moment. After a turbulent stretch defined by sweeping tariffs, a lengthy federal government shutdown, and energy price shocks tied to Middle East tensions, the American economy has demonstrated a quiet resilience that has surprised even seasoned forecasters. Growth is holding, workers are still earning more than inflation takes away, and businesses are investing at rates not seen in years. Yet none of this means smooth sailing — affordability pressures persist, the job market has cooled noticeably, and the Federal Reserve is navigating a narrow path between taming inflation and protecting employment. This article breaks down where the US economy stands heading into the summer of 2026, what the key data tell us, and what everyday Americans can realistically expect in the months ahead.

Background: How We Got Here

To understand the current US economy update, it helps to trace the road that led to June 2026. The economy entered the year carrying several heavy burdens. A six-week federal government shutdown in late 2025 disrupted official data collection — the October unemployment and inflation figures were never calculated, leaving policymakers and analysts navigating in something of an information blackout. Simultaneously, a broad round of tariff increases took effect in April 2026, reshaping trade flows in dramatic fashion. Businesses front-loaded imports in Q1, causing import figures to spike at a 38% annualized rate before snapping back sharply in Q2. This import volatility created wild swings in the headline GDP figures, making it harder to assess the economy’s true underlying strength. Add in elevated energy prices driven by the Iran conflict and the picture becomes complex — but not catastrophic. The economy’s foundations — consumer spending, business investment, and the labor market — have proven more durable than many feared.

The State of the US Economy: Key Developments

GDP Growth: Moderate Expansion Continues

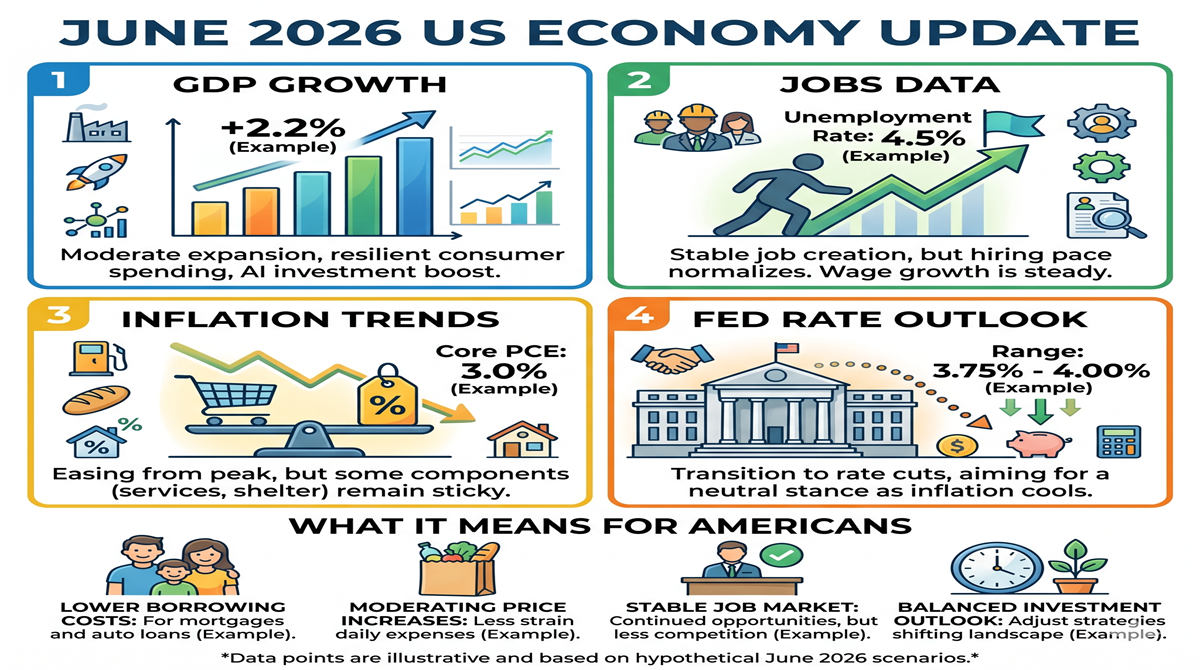

Real GDP growth came in at 2.0% at an annual rate in Q1 2026, a rebound from the sluggish 0.5% recorded at the close of 2025. Full-year growth forecasts for 2026 cluster in the 1.8%–2.4% range, depending on the forecaster and assumptions about tariff impacts and global energy markets. The US Treasury has characterized the economic landscape as favorable, pointing to robust business investment — up more than 10% in Q1 2026 — driven by spending on new equipment and intellectual property, including a surge of AI-related capital expenditure. The US Chamber of Commerce notes that AI investment alone is keeping investment figures elevated and sustaining employment across a wide range of sectors. While this growth pace is below the post-pandemic boom years, it represents steady, sustainable expansion rather than the sharp contraction that recession fears had predicted just a year ago. The probability of a recession over the next 12 months has dropped to roughly 30%, down from an earlier estimate of 40%, according to RSM US economists.

Labor Market: Resilient but Clearly Cooling

The jobs picture in mid-2026 tells a story of a labor market that has shifted decisively into lower gear. Monthly job gains have averaged around 75,000, compared to 167,000 per month in 2024 — a steep drop that reflects both slower business expansion and the dampening effects of tariff uncertainty on hiring plans. The unemployment rate is expected to hover between 4.5% and 4.8% through the year. Private sector payroll growth in Q1 2026 did surge to more than 2.5 times the monthly average seen in 2025, offering a brighter data point, but analysts caution against reading too much into a single quarter. On the positive side, wage growth continues to outpace inflation, meaning that workers who have jobs are seeing their real purchasing power rise. Layoffs remain historically low, and the labor market has settled into what Stanford economists describe as a “low-hire, low-fire equilibrium” — stable but not dynamic. For job seekers, this translates to a tougher environment than 2022 or 2023, with fewer openings and slower wage bidding among employers.

Inflation and the Fed: Cautious Optimism

Inflation remains above the Federal Reserve’s 2% target, with the consumer price index running at approximately 2.7% on a 12-month basis. Energy prices, elevated by the Iran conflict, have nudged headline inflation higher than it might otherwise be. However, the Fed and independent analysts take some comfort in the underlying trends: core inflation is moderating, housing costs are coming down, and long-term inflation expectations remain well-anchored. A Philadelphia Federal Reserve official has described the outlook for inflation as one of “cautious optimism,” noting that there is a plausible path to 2% core inflation by year-end on a run-rate basis. As for interest rates, the Fed has signaled it is in no hurry to cut. Most forecasters do not expect a rate reduction before September 2026 at the earliest, as policymakers wait for clearer signs that both inflation and employment risks are balanced. The Congressional Budget Office projects inflation will slow to 2.7% in 2026 and return to the Fed’s 2% goal by 2030.

📌 Key Points: US Economy June 2026

- Real GDP grew at a 2.0% annual rate in Q1 2026, recovering from a near-stall at the end of 2025, with full-year growth expected between 1.8% and 2.4%.

- Business investment surged more than 10% in Q1 2026, fueled by AI spending and new equipment purchases, acting as a key engine of economic growth.

- The labor market has cooled significantly, with monthly job gains averaging around 75,000 — less than half the pace seen two years ago — while unemployment sits near 4.5%–4.8%.

- Inflation remains above target at roughly 2.7%, with energy price pressures from the Middle East conflict complicating the Federal Reserve’s path toward rate cuts.

- Worker wages are still outpacing inflation, providing a modest but important cushion for household finances even as cost-of-living pressures persist.

Impact & Analysis: What This Means Going Forward

The broader implications of this US economy update are mixed but leaning cautiously constructive. For consumers, the good news is that real wages are positive — dollars earned are still buying more than a year ago, even if the margin of comfort is thin. Mortgage rates remain elevated, keeping the housing market sluggish and homeownership out of reach for many younger Americans. Tariffs continue to filter through into goods prices, adding a steady drip of cost pressure that falls disproportionately on lower-income households who spend a larger share of income on imported goods and food.

For businesses, the picture is brighter. Investment is strong, credit markets remain functional, and AI adoption is creating real productivity gains in certain sectors. The longer-term outlook hinges on whether AI delivers on its promise of broader productivity growth. Goldman Sachs analysts have estimated that generative AI could create up to $8 trillion in value for US firms through labor efficiency gains — if that materializes, current growth trajectories could meaningfully accelerate. In the short term, however, uncertainty around tariffs, energy prices, and Fed policy means businesses are likely to stay cautious on large commitments. The economy in mid-2026 is one of slow but steady expansion — not exciting, but also not breaking down.

People Are Also Asking

Conclusion

The US economy update for June 2026 paints a portrait of a nation that has weathered significant storms — tariff shocks, a government shutdown, global conflict — and come out the other side still standing, if a little worn. GDP growth is modest but real. Business investment is surprisingly strong. Workers are still ahead of inflation. The challenges are genuine: inflation lingers above target, the job market has lost its former dynamism, housing remains unaffordable for millions, and global risks haven’t disappeared. But the doomsday scenarios that loomed large a year ago have not materialized. The outlook for the remainder of 2026 is cautious expansion — not a boom, but not a bust either. If you found this breakdown useful, share it with someone trying to make sense of today’s economic headlines, and drop your questions in the comments below.

⚠️ This article is for informational purposes only and does not constitute financial or investment advice. Data and forecasts referenced are sourced from the US Department of the Treasury, RSM US, Purdue University Extension, Stanford Institute for Economic Policy Research (SIEPR), the Indiana Business Research Center, the Congressional Budget Office, and the US Chamber of Commerce. Figures reflect the most current publicly available data as of late May 2026.

Related Internal Links

- Best High-Yield Savings Accounts June 2026

- HP ProBook 640 G5 Review: Is It Worth Buying in 2026

- SlimLeaf Reviews 2026: Does ingredients, benefits, side effects, pricing,

- Glycovit Reviews: Does This Blood Sugar Supplement Work