Best High-Yield Savings Accounts June 2026: Earn Up to 5.00% APY

| Label | Value |

|---|---|

| Topic | Best High-Yield Savings Accounts for June 2026 |

| Key Figures | Top APY: 5.00% (Varo Bank); Best no-fuss rate: 4.03% (Vio Bank); National average: 0.38% |

| Who It Affects | Anyone looking to grow emergency funds or short-term savings in a low-risk account |

| Time Period | Rates current as of late May 2026; Fed next meets June 17, 2026 |

| Bottom Line | Top HYSAs still earn roughly 10× the national average — act before potential rate cuts narrow the window further |

Introduction

If your savings are still sitting in a traditional bank account earning a fraction of a percent, you are leaving real money on the table. The best high-yield savings accounts in June 2026 are offering annual percentage yields (APYs) of up to 5.00% — a figure that dwarfs the national average of just 0.38%. Whether you are building an emergency fund, saving toward a big purchase, or simply want your idle cash working harder, a high-yield savings account (HYSA) is one of the smartest, lowest-risk moves you can make right now.

In this guide, we break down the top-performing HYSAs heading into June 2026, explain what to look for when choosing one, and help you understand how the Federal Reserve’s current stance is shaping the savings landscape. Rates are still strong — but the window may not stay open forever.

Background: How We Got Here

To understand why today’s savings rates are so attractive, it helps to look back. Beginning in 2022, the Federal Reserve launched an aggressive rate-hiking cycle to bring inflation under control. By 2023, top HYSAs were routinely clearing 5% APY — a level not seen in over a decade. Then, in late 2024, the Fed began cutting rates as inflation cooled, and savings yields started to ease downward.

Fast-forward to today: the Fed has held the federal funds rate steady at a target range of 3.50%–3.75% through three consecutive meetings in 2026 — including most recently on April 29. The next rate decision is due June 17, 2026. This pause has given savings rates a moment to stabilize after months of gradual decline. The national average has slipped slightly to 0.38%, but the gap between that benchmark and the rates offered by online-first banks remains enormous. For savers, this pause is a genuine opportunity — but one that could narrow if the Fed resumes cuts later in the year.

Top High-Yield Savings Accounts for June 2026

🏆 The Highest APY: Varo Bank — Up to 5.00%

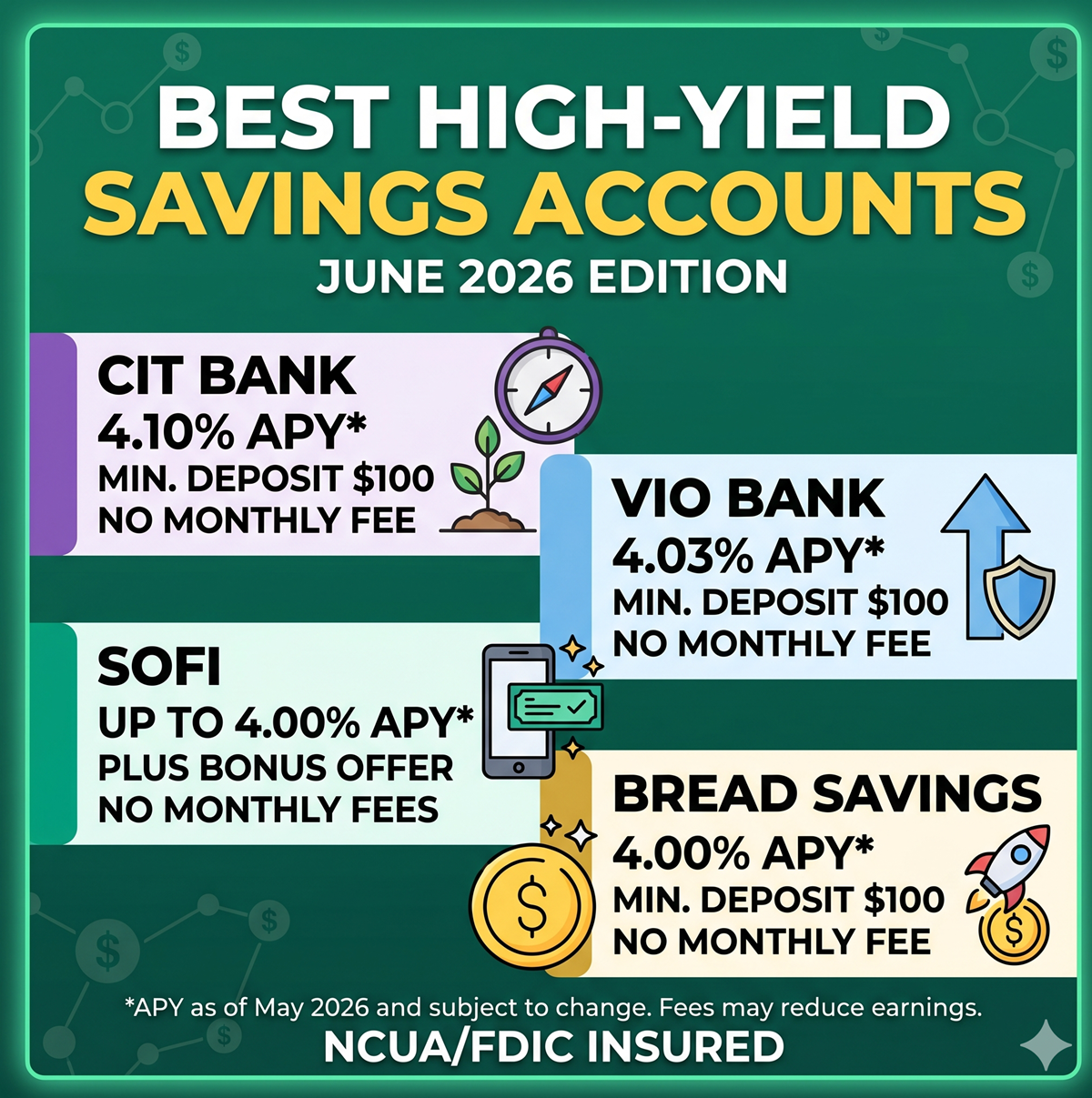

Varo Bank continues to lead the pack with an eye-catching 5.00% APY — but there are conditions attached. To earn the headline rate, customers must receive at least $1,000 in direct deposits each month and maintain a positive account balance. The 5.00% APY applies only to balances up to $5,000; amounts above that threshold earn 2.50%. For savers who can meet those requirements, however, Varo is an outstanding choice. It also bundles useful automatic savings tools — like rounding up purchases to the nearest dollar and sweeping the difference into savings — making it easier to hit your balance goals without thinking about it. There are no monthly fees, which keeps the value proposition clean.

💡 Best for Accessibility: Vio Bank — 4.03%

If you want a strong rate without hoops to jump through, Vio Bank is the standout pick. Its savings account earns 4.03% APY with minimal minimum deposit requirements — no direct deposit mandate, no monthly balance thresholds. Vio Bank is the online division of MidFirst Bank, the largest privately held bank in the United States, lending it a layer of institutional credibility that some newer fintech players lack. For savers who want simplicity and a genuinely competitive yield, Vio Bank is among the cleanest options on the market.

📲 Strong Alternatives Worth Knowing

Beyond the two leaders, several other accounts deserve attention depending on your priorities:

- SoFi Checking and Savings: Earns 3.30% APY with eligible direct deposit, rising to up to 4.00% APY for the first six months with a promotional boost. No monthly fees, and new members can earn a cash bonus. Works best as a combined checking-and-savings solution.

- American Express High Yield Savings: Sitting at 3.10% APY as of late May 2026, Amex’s account won’t win a rate contest, but it offers the rock-solid reliability of a major financial brand, zero minimum balance, and no fees — appealing for savers who prioritize trust and simplicity.

- Axos ONE® Savings: Offers a highly competitive APY on balances up to $249,999. Customers get access to over 95,000 fee-free ATMs, though a higher-than-average minimum deposit of $250 applies to open the account.

- Marcus by Goldman Sachs: A perennial favorite for no-fee savings with a straightforward rate and the backing of Goldman Sachs. Ideal for savers who want a name they recognize alongside a strong yield.

- CIT Bank Platinum Savings: Well-suited for those with larger balances, this account tiers its APY to reward higher deposits — and a current promotional boost (running through June 30, 2026) adds an extra 0.35% APY for new account holders.

📌 Key Points at a Glance

- Top HYSAs in June 2026 offer APYs up to 5.00%, roughly 13 times the national average of 0.38%.

- The Federal Reserve held rates steady at 3.50%–3.75% in April 2026, giving savings yields a period of stability after months of gradual decline.

- Varo Bank leads on raw APY (5.00%) but requires monthly direct deposits of $1,000 and caps the high rate at $5,000 in balances.

- Vio Bank offers the strongest no-strings-attached rate at 4.03% APY with minimal requirements, making it accessible to most savers.

- The Fed’s next rate decision on June 17, 2026 could shift the savings landscape — locking in a strong rate now is a smart precaution.

Impact & Analysis: What This Means for Savers

In practical terms, the gap between a traditional savings account and a top HYSA is substantial. On a $10,000 balance, earning 0.38% (national average) generates just $38 in interest over a year. At 4.03% (Vio Bank), that same balance earns roughly $403 — more than ten times as much. At 5.00% on a $5,000 balance, Varo delivers $250 in annual interest on those funds. None of these accounts require you to lock your money away or take on investment risk.

The short-term outlook is cautiously optimistic for savers. The Fed’s three consecutive pauses suggest policymakers are in no rush to cut rates further, which should keep HYSA rates relatively stable through the summer. That said, many economists still expect one or two rate cuts later in 2026, which would translate into lower savings yields. The longer-term trend for savings rates is likely downward from current highs.

Anyone who has been delaying opening a high-yield savings account should treat the period before the June 17 Fed announcement as a natural deadline to act. Even if rates hold steady, waiting means missed interest. If the Fed signals cuts, rates could slip within weeks.

People Are Also Asking

Conclusion

The best high-yield savings accounts heading into June 2026 continue to offer returns that blow traditional banking out of the water. With rates up to 5.00% still available and the Federal Reserve in a holding pattern, now remains a genuinely strong time to be a saver. Varo Bank leads on maximum yield, Vio Bank wins on accessibility, and strong alternatives from SoFi, Axos, Marcus, and American Express cover a wide range of savers’ needs and habits.

The key is to act before the landscape shifts. The Fed’s June 17 meeting could bring news that nudges rates lower. Even a small delay costs you real interest. Take ten minutes today to compare your options, pick an account that fits your habits, and let your savings start working as hard as you do. If you found this guide helpful, share it with someone whose money deserves better than 0.38% APY.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. APYs and account details are subject to change. Always verify current rates directly with the financial institution before opening an account.

Sources: NerdWallet (May 22, 2026), CBS News, CNBC Select, The Motley Fool, Fortune, Doctor of Credit — rates referenced as of late May 2026.

Related Internal Links

- HP ProBook 640 G5 Review: Is It Worth Buying in 2026

- SlimLeaf Reviews 2026: Does ingredients, benefits, side effects, pricing,

- Glycovit Reviews: Does This Blood Sugar Supplement Work

- NeuroVera Reviews 2026: A Complete, Honest Look at the Brain Supplement Everyone Is Talking About